[2013] ATP 5

Catchwords:

Decline to conduct proceedings – contract dispute – disclosure – material omission – unsolicited bid - bidder’s statement – liquidity event - efficient, competitive and informed market – equal opportunity – shareholder approval – withdrawal rights – undertaking – compulsory acquisition

Corporations Act 2001 (Cth) section 602, item 7 of section 611 and sections 636(1)(m), 659B, 661A, 662A

Lionsgate Australia v Macquarie Private Portfolio [2007] NSWSC 318, Tower Software Engineering; Pendant Software v Harwood and others (2006) 57 ACSR 653

| Interim order | IO undertaking | Conduct | Declaration | Final order | Undertaking |

|---|---|---|---|---|---|

| No | Yes | No | No | No | No |

Introduction

- The Panel, Martin Alciaturi, Diana Chang (sitting President) and Alison Watkins, declined to conduct proceedings on an application by Jiggi Investments Pty Ltd and others in relation to the affairs of Careers Australia Group Limited. The application concerned a bid by Cirrus Business Investments Limited for all the shares in Careers Australia and, primarily, whether a clause in the Convertible Note Deed entered into by Careers Australia and Cirrus in 2011 required that Cirrus’ bid be subject to approval by non-associated shareholders of Careers Australia or the independent board committee formed to consider the bid. The Panel considered that there was no reasonable prospect that it would declare the circumstances unacceptable.

- In these reasons, the following definitions apply.

Applicants

Jiggi Investments Pty Ltd ATF Graham and Company Executive Superannuation Fund, Wayburn Holdings Pty Ltd, Vernon and Jillaine Wills ATF the Wills Family Super Fund, Vernon Wills and Jillaine Wills, D & E Somerville ATF Sommerville Super Fund, Ganbros Pty Ltd, Jim and Lisa Elder ATF Elder Superannuation Fund, Orbit Capital Pty Ltd, Devine Superannuation Pty Ltd ATF Devine Executive Super Fund, Depofo Pty Ltd ATF Super account, Depofo Pty Ltd ATF Depofo TT account, Pinbrook Pty Ltd, Myall Resources Pty Ltd ATF Myall Unit A/C, Myall Resources Pty Ltd ATF Myall Super A/C and Onmell Pty Ltd ATF Brent Potts Super Fund A/C

Careers Australia

Careers Australia Group Limited

Cirrus

Cirrus Business Investments Limited

Deed

the Convertible Note Deed between Careers Australia and Cirrus under which Careers Australia issued 60.6 million convertible notes with a face value of $40 million to Cirrus

White Cloud

White Cloud Capital Fund Limited

Facts

- Careers Australia is an unlisted public company with approximately 63 shareholders. The Applicants are shareholders that hold “well in excess of 10%” of Careers Australia.

- On 12 May 2011, Careers Australia and White Cloud1 entered into a heads of agreement in relation to an investment in Careers Australia. On 12 July 2011, Careers Australia and Cirrus (controlled by White Cloud) entered into the Deed.

- On 13 July 2011, Careers Australia shareholders approved Cirrus acquiring a relevant interest of up to 45.29% in Careers Australia through the conversion of the convertible notes.

- Cirrus has converted most of the convertible notes and holds a 45.2% interest in Careers Australia. If the remainder of its convertible notes were converted, Cirrus would hold a 47.2% interest in Careers Australia.

The Deed includes clause 14.3, which states:

“The Company [Careers Australia] and the Noteholder [Cirrus] acknowledge and agree that, subject to the ongoing duties of the Directors and without fettering any discretion the Directors have, the Company will consider either an initial public offering and listing on the Australian Securities Exchange (IPO) or another form of liquidity event with a period of 2 years from the Issue Date and the parties undertake to take all reasonable steps to effect the IPO or other form of liquidity event provided that such action is considered to be in the best interests of all the Company security holders at that time. In the event that the Directors, acting in the best interests of the Company security holders elect not to proceed with an IPO or other form of liquidity event at that time the Directors shall consider at least annually thereafter whether an IPO or other form of liquidity event would be in the best interests of the Company security holders at that time.” (emphasis in original)

- On or about 3 May 2013, Careers Australia received a takeover proposal from Cirrus offering $0.66 per share. Cirrus served its bidder’s statement on Careers Australia on 22 May 2013. The offer was not solicited.

- The offer does not include a minimum acceptance condition and is not subject to Careers Australia shareholder approval.

- Cirrus’ bidder’s statement refers to the offer as a “liquidity event” and states that “Cirrus and Careers Australia also agreed to consider a liquidity event within two years [of the convertible note investment].” The bidder’s statement says that Cirrus:

- does not have plans to offer Careers Australia shareholders an additional future liquidity event

- believes than an initial public offering would not be in the best interests of Careers Australia and all its shareholders and it does not plan to support a listing on ASX or any other financial market

- has no intentions to sell its Careers Australia shares and intends to be a long term holder and

- does not intend to compulsorily acquire Careers Australia shares if it becomes entitled to do so at the end of the offer period.

- In a supplementary bidder’s statement dated 5 June 2013, Cirrus clarified that if it achieves a 90% relevant interest in Careers Australia it will comply with s662A(1)2 and make buy-out offers to remaining shareholders.

- In accordance with the heads of agreement, 3 of the 6 directors on the Careers Australia board (Jonas Martin- Löf, Errol Clark and Robert Mansfield) are nominees of White Cloud.

- Jonas Martin Löf is a common director between Careers Australia and Cirrus. Errol Clark is part of White Cloud’s investment advisory team and a director of White Cloud. Robert Mansfield is a senior advisor of White Cloud.

- Careers Australia has formed an independent board committee – Shane Edwards and Ian Grier - to consider Cirrus’ offer.

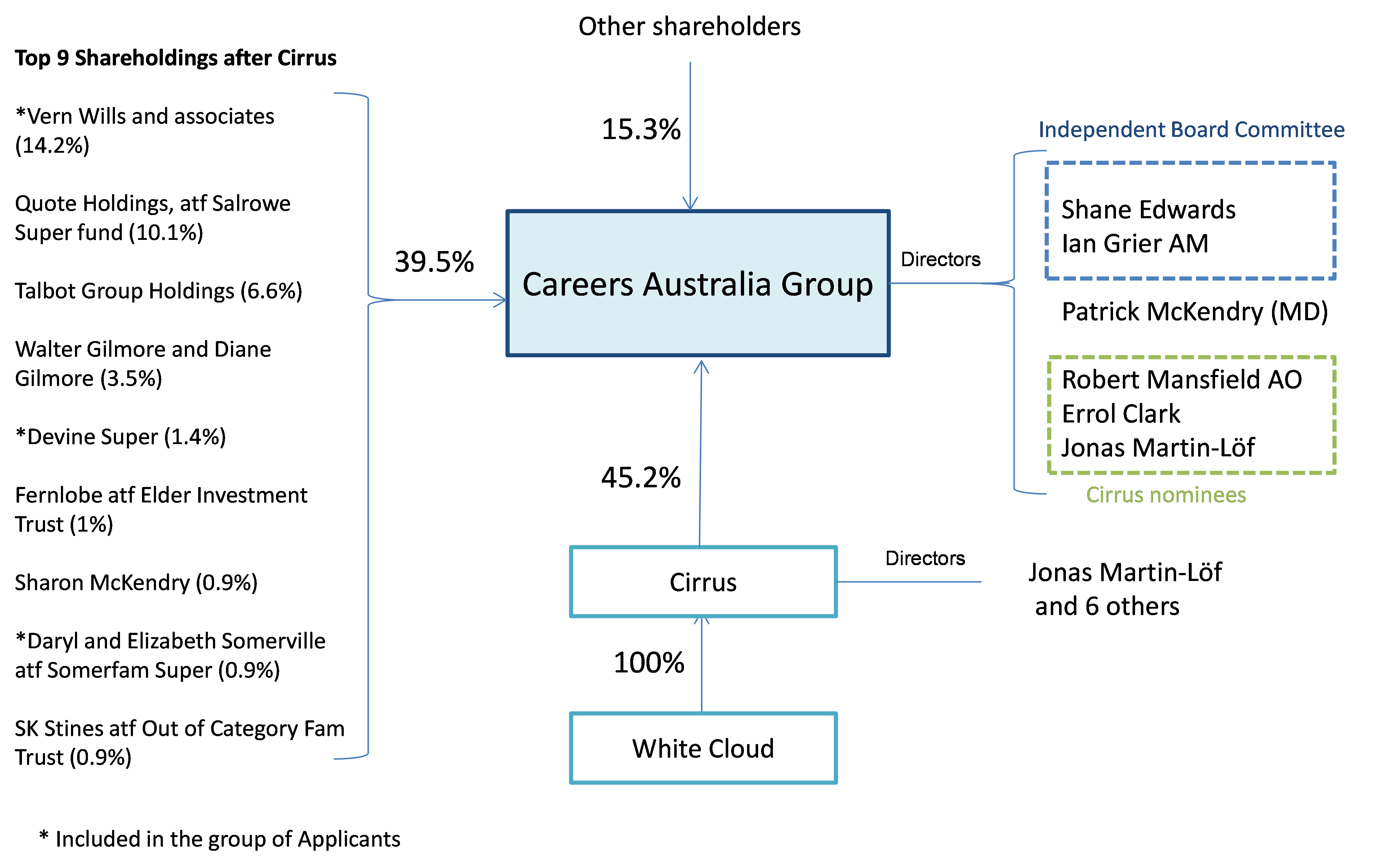

Various relationships are shown in the following diagram:

Text description

This chart shows various individuals and companies which have relationships with Careers Australia Group.

White Cloud owns 100% of Cirrus, which owns 45.2% of the shares in Careers Australia Group. The directors of Cirrus are Jonas Martin-Löf and 6 others.

The top 9 shareholders after Cirrus own 39.5% of the shares in Careers Australia Group. The top 9 shareholders are as follows: Vern Wills and associates (14.2%), Quote Holdings as trustee for Salrowe Super Fund (10.1%), Talbot Group Holdings (6.6%), Walter Gilmore and Diane Gilmore (3.5%), Devine Super (1.4%), Fernlobe as trustee for Elder Investment Trust (1%), Sharon McKendry (0.9%), Daryl and Elizabeth Somerville as trustee for Somerfam Super (0.9%), and SK Stines as trustee for Out of Category Fam Trust (0.9%).

The remaining shareholders own 15.% of the shares in Careers Australia Group.

The directors of Careers Australia Group fall within three categories: (1) Shane Edwards and Ian Grier AM (who form the Independent Board Committee), (2) Patrick McKendry, and (3) Robert Mansfield AO, Errol Clark, and Jonas Martin-Löf (who are the Cirrus nominees).

- Careers Australia appointed an independent expert as required by s640(1), Crowe Horwath, which concluded that the Cirrus offer was neither fair nor reasonable. The independent expert valued Careers Australia shares in the range $0.85 - $0.96.

- Careers Australia released its target’s statement on 12 June 2013, recommending that shareholders reject Cirrus’ offer.

Application

Declaration sought

- By application dated 11 June 2013, the Applicants sought a declaration of unacceptable circumstances.

- The Applicants submitted that in effect clause 14.3 of the Deed implied an obligation for Cirrus to seek non-associated (Careers Australia) shareholder, or independent board committee, approval for its offer. The Applicants submitted that the unsolicited bid meant that Cirrus did not intend to comply with clause 14.3 and, therefore, because acceptances in respect of 5% would take Cirrus to more than 50% of Careers Australia, it may acquire control over voting shares other than in an efficient, competitive and informed market. Moreover, with a closing date of one month after the offers were made, the offer period did not give Careers Australia shareholders a reasonable time to consider the offer.

- The Applicants also submitted that Cirrus made no disclosure of clause 14.3 in its bidder’s statement.

- The Applicants also submitted that because Cirrus did not intend to offer an additional liquidity event and did not intend to compulsorily acquire shares if it became entitled to do so, shareholders were denied a reasonable and equal opportunity to participate in benefits accruing to shareholders who do accept the offer.

Interim orders sought

- The Applicants sought interim orders, pending determination of their application, including to the effect that Cirrus not process any acceptances from Careers Australia shareholders prior to shareholder approval of Cirrus’ offer and that a withdrawal right be offered to accepting shareholders prior to shareholder approval.

- Cirrus provided an undertaking (see Annexure) to the effect that, until the happening of certain events, it would not cause its offer to become unconditional without giving the Panel and parties at least 2 business days’ notice. On this basis, the acting President declined to make interim orders. However, he noted that it was open to the sitting Panel to re-consider the issue of interim orders.

- Because we have declined to conduct proceedings, the undertaking is no longer in effect.

Final orders sought

- The Applicants sought final orders, including to the effect that Cirrus disclose clause 14.3 and the rights of shareholders under it, that Cirrus be directed to comply with clause 14.3 in relation to the offer, that Cirrus’ offer be subject to non-associated Careers Australia shareholder or independent board committee approval, and that the offer be extended and a withdrawal right be provided to shareholders who accepted prior to shareholder (or independent board committee) approval.

Notice of appearance from Quote Holdings Pty Ltd

- Quote Holdings Pty Ltd as trustee for the Salrowe Superannuation Fund submitted a notice of appearance in relation to this matter. As we have declined to conduct proceedings we do not accept the notice of appearance.

Preliminary submissions

- White Cloud made preliminary submissions that, among other things, the Applicants were not parties to the Deed and had no legal standing to allege a breach of its terms. It also submitted that the Panel does not have jurisdiction in relation to an alleged breach of contract between Cirrus and Careers Australia. It also submitted that Cirrus had complied with its obligation under the Deed.

Discussion

Jurisdiction

- The Applicants had submitted in the application that “there are a number of examples of the Panel declaring that unacceptable circumstances exist, even where a corporate act may not offend Chapter 6 or may be expressly within an exception contained in Section 611 of the Corporations Act.”

- The Applicants responded to White Cloud’s preliminary submission noting that the Panel has wide jurisdiction and may examine circumstances relating to contractual matters where the transaction is likely to have an effect on the efficient, competitive and informed market for control of a company.3

- While what the Applicants submitted is true, it is necessary for circumstances to offend the purposes of Chapter 6 set out in s602 or other policy underpinning the provisions of Chapters 6-6C, or for there to be another relevant public policy issue, before the Panel is the appropriate forum to consider the matter.

In Lionsgate Australia v Macquarie Private Portfolio4 the court considered whether, having regard to s659B, a bidder could commence court proceedings for specific performance of its contract with a substantial shareholder of the target. The court found that s659B did not preclude the bidder seeking specific performance of its contract, adding that the Panel may also consider the matter:

Those provisions establish that a contract for the sale of shares in a company is capable of falling within the affairs of the company itself. Moreover, here the circumstances to which the panel would be expected to have regard, if an application were made to it, would not be limited to the sale of the company’s shares per se. The relevant circumstances would include the fact that the seller is a substantial shareholder, that the sale was entered into in anticipation of a takeover bid, and that the contractual obligation is to sell into the bid, triggered by the posting of the bidder’s statement. These matters bring a transaction that might, conceivably, be regarded as a private transaction, remote from the company itself, within the ambit of matters affecting the company in connection with its membership, the ownership of shares, and control over voting and disposal of shares. That being so, I am satisfied that the circumstances which are the subject of, and surround, Lionsgate’s court proceedings for specific performance, when taken together, constitute affairs of Magna Pacific for the purpose of a panel application for a declaration that those circumstances are or include unacceptable circumstances.

In summary, while the proper construction of s659B is affected by considering the panel’s power to deal with the subject-matter of the court proceedings or circumstances including that subject-matter, here it has not been shown that the panel would lack the power to entertain an application. This part of Lionsgate’s argument as to the scope of s659B is unsuccessful, but Lionsgate succeeds on the proper construction of s659B(4), for the reasons given above.5

- In Tower Software Engineering; Pendant Software v Harwood and others6 the court acknowledged that the Panel and the court may consider matters deriving from the same circumstances contemporaneously, noting that it was for the court to determine whether a breach of s1071F had occurred (in that case) but for the Panel to determine whether there were unacceptable circumstances in relation to a takeover offer.

- While the Panel may have jurisdiction to consider a contract, there would need to be a relevant nexus between the contract terms and their effect on control of a company7 before the Panel would become involved. For the reasons set out below, we do not consider that to be the case here.

Clause 14.3 of the Deed

- The Applicants submitted that clause 14.3 imposed an obligation on Cirrus and Careers Australia to “pursue conduct which was designed to provide all CAG Shareholders with the opportunity of being able to realise the value of their investment in CAG through pursuit of a liquidity event in the form of either an IPO and stock exchange listing or some other liquidity event and not to simply act unilaterally without reference to or consultation with one another.”

- We do not think that clause 14.3 implies an obligation on Cirrus as the Applicants contend, but even if it did, the offer does not give rise to unacceptable circumstances.

- The making of an offer that complies with Chapter 6 and meets the purposes set out in s602 is not an event that we should ordinarily interfere with, and in this case we see nothing that makes the offer unacceptable.

- It is the nature of a bid that all shareholders have their say, because each shareholder is free to accept or reject it. It is unclear why, in this case, that freedom should be curtailed. Even if it is the case that a majority of the non-associated shareholders do not wish to accept the offer, there is no reason why they should constrain the minority.

- We do not see any reason why the statutory minimum bid period of 1 month is inadequate in this situation.

Disclosure regarding clause 14.3 of the Deed

- The Applicants submitted that Cirrus contravened s636(1)(m) because it did not disclose clause 14.3 in its bidder’s statement.

- White Cloud made preliminary submissions that there was no breach of s636(1)(m) because clause 14.3 had previously been disclosed to shareholders as part of the item 7 of s611 approval in 2011 and Careers Australia’s register had not changed since.

- We doubt that disclosure 2 years ago is sufficient, but we do not need to decide that because we do not consider clause 14.3 imposes the obligation on Cirrus in relation to its offer that the Applicants contend. Accordingly, the materiality of disclosure regarding it falls away. In any event, Careers Australia’s target’s statement8 provided additional disclosure about clause 14.3 so any information deficiency has been remedied.9

Cirrus’ intention not to pursue compulsory acquisition

- A bidder may become entitled to proceed to compulsory acquisition at the conclusion of its bid. Cirrus stated in its bidder’s statement that it did not intend to proceed to compulsory acquisition if it became entitled to do so.

- In a supplementary bidder’s statement Cirrus stated that it would be obliged to offer to buy out the remaining shareholders if it achieved a relevant interest of at least 90% in Careers Australia shares at the end of the offer period.10

- In our view Cirrus has not denied shareholders a reasonable and equal opportunity to participate in the benefits accruing to shareholders who do accept the offer. Shareholders have the opportunity to accept the offer and, if s662A applies, shareholders who have not accepted will also have the right to be bought out. This has been adequately disclosed through the bidder’s statement, supplementary bidder’s statement and target’s statement.

- While circumstances may exist where the intention not to proceed to compulsory acquisition would coerce shareholders in a way that gives rise to unacceptable circumstances (which we think would be rare in any event) they do not appear to exist here.

Decision

- For the reasons above, we do not consider that there is any reasonable prospect that we would make a declaration of unacceptable circumstances. Accordingly, we have decided not to conduct proceedings in relation to the application under regulation 20 of the Australian Securities and Investments Commission Regulations 2001 (Cth).

Orders

- Given that we have decided not to conduct proceedings, we do not (and do not need to) consider further whether to make an interim order.

- Given that we made no declaration of unacceptable circumstances, we make no final orders, including as to costs.

Diana Chang

President of the sitting Panel

Decision dated 20 June 2013

Reasons published 21 June 2013

Advisers

| Party | Advisers |

|---|---|

| Applicants | HopgoodGanim |

| Cirrus Business Investments Limited and White Cloud Capital Advisors Limited in its capacity as advisor of White Cloud Capital Fund | Minter Ellison |

| Careers Australia Group Limited | Herbert Smith Freehills |

Annexure

Australian Securities and

Investments Commission Act 2001 (Cth) Section 201A

Undertaking

Careers Australian Group Limited 02

Cirrus undertakes to the Panel that it will give the Panel and the parties to the proceedings no less than 2 business days’ notice before causing its offers to become unconditional.

This undertaking ends on the earliest of:

- the Panel deciding not to conduct proceedings

- if the Panel decides to conduct proceedings, the determination of those proceedings or

- the date that is 3 business days before the date on which notice under section 630(3) of the Corporations Act 2001 (Cth) is required to be given.

Cirrus agrees to confirm in writing to the Panel when it has satisfied its obligations under this undertaking.

In this undertaking:

Cirrus means Cirrus Business Investments Limited.

offers means the off-market takeover offers for all the shares of Careers Australia Group Limited included in Cirrus’ bidder’s statement dated 22 May 2013.

proceedings means the Panel proceedings brought by application dated 11 June 2013 by Jiggi Investments Pty Ltd and others.

Signed by Jonas Martin-Löf

with the authority, and on behalf, of

Cirrus Business Investments Limited

Dated 14 June 2013

1 Through its advisor, White Cloud Capital Advisors Limited

2 References are to the Corporations Act 2001 (Cth) unless otherwise specified

3 Although the Applicants’ response was outside the process we accepted it

4 [2007] NSWSC 318

5 At [54] – [55]

6 (2006) 57 ACSR 653

7 Section 657A(2)(i). An effect in terms of s657A(2)(a)(ii), (b) or (c) would also meet this test

8 See section 5 of the target’s statement

9 We understand there had been no acceptances at the date of the target’s statement

10 S662A