[2003] ATP 16

Catchwords:

Relevant interest acquired through restructure of US-based debt - ownership and control of controlling shareholder - disclosure of shareholders agreement - undocumented agreement - insufficient disclosure of intentions - timing for disclosure of intentions - uninformed market - substantial shareholder notice - ASIC relief - identity and standing of applicant

Corporations Act 2001 (Cth), sections 606(1), 671B(4) and 602(a)

These are our reasons for declining to make a declaration of unacceptable circumstances in response to an application under section 657C of the Corporations Act by Pondale Properties Pty Limited (Application). The Application was for a declaration of unacceptable circumstances in connection with the acquisition by CHAMP SPV Pty Limited and its related entities (CHAMP Group) of a relevant interest of approximately 81% in the share capital in Austar United Communications Limited (Austar).

Preliminary

- The sitting Panel is made up of Nerolie Withnall (sitting President), Alice McCleary (sitting Deputy President) and Michael Ashforth.

Summary

- Pondale, a shareholder in Austar, applied to the Panel on 28 February 2003 for a declaration of unacceptable circumstances in relation to the acquisition by CHAMP Group of a relevant interest in approximately 81% of the shares in Austar.

- The CHAMP Group acquired the relevant interest in the Austar shares through funding a US Chapter 11 debt restructure of a subsidiary of United Asia/Pacific Communications Inc (UAPC). At the time of the Application, UAPC had a relevant interest in approximately 81% of the shares in Austar.

- Pondale asserted in the Application that the market for Austar shares was not adequately informed about the ultimate ownership and control of the CHAMP Group. It alleged that the acquisition by the CHAMP Group of a controlling interest in Austar would not take place in an efficient, competitive and informed market.

- The Panel declined the Application on 18 March 2003 although it considered that the applicant had made out some of its concerns. However, the Panel believed that those concerns were addressed by:

- the issue by CHAMP Group of a detailed media release on 5 March 2003; an

- the disclosure of an agreement between the future controllers of 81% of Austar in supplementary substantial shareholding notices on 13 March 2003.

- The Application also raised concerns about Pondale, which appeared to be instructed to make the Application on behalf of another entity, details of which were not disclosed at the time the Application was made.

Relevant Parties

- Austar is a company listed on the Australian Stock Exchange. Its principal business activity is delivering subscription television services to regional Australia.

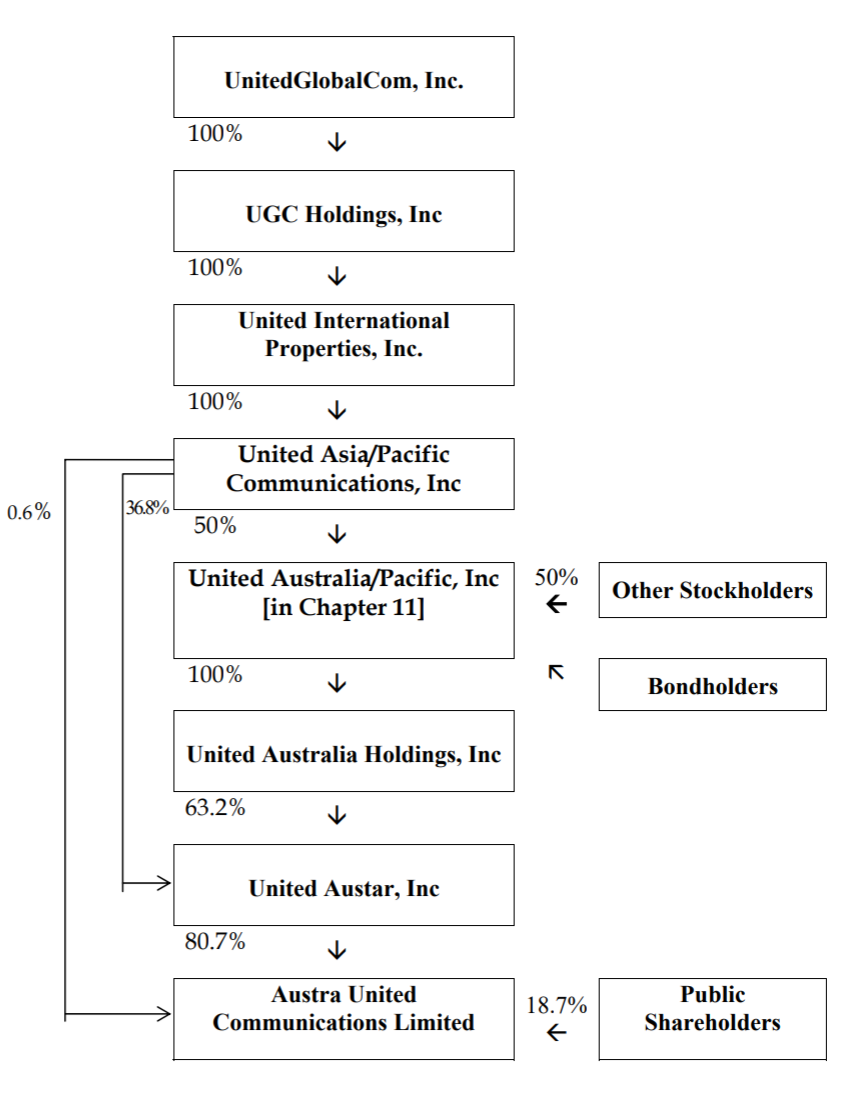

- At the time the Application was made, Austar had the following shareholders:

Shareholder Shareholding (%) Nationality United Austar Inc (UAI)

80.7

United States

United Asia/Pacific Communications Inc (UAPC)

0.6

United States

Other (widely held)

18.7

Predominantly Australian

- UAPC is ultimately held by United Global Com Inc. When the Application was made, UAI was also ultimately held by United Global Com Inc by means of a chain of companies in that UAI was 63.2% owned by United Australia Holdings Inc (UAH) and 36.8% owned by UAPC. UAH is 100% held by United Australia/Pacific Inc (UAP), which is in turn owned as to 50% by UAPC. These companies are together referred to as the UGC Group. A diagram of these shareholdings is set out at Appendix A.

- Castle Harlan Australian Mezzanine Partners Pty Limited (CHAMP) is a private equity funds manager, the beneficial investors of which are predominantly superannuation funds and institutional investors. No investor has more than 20% in a CHAMP Group fund. Mr. Bill Ferris and Mr. Joseph Skrzynski and their respective families, John Castle and Leonard Harlan ultimately beneficially own CHAMP.

- Pondale Properties Pty Limited (Pondale) is a small private company, in which the solicitor acting for Pondale was a shareholder. The only other shareholder in Pondale was married to the solicitor acting for Pondale. Watson Mangioni is the firm of solicitors acting for Pondale.

Background

- Austar's operations have suffered and continue to suffer losses. Its share price has fallen from $9.90 at the commencement of 2000 to 14 cents in the second half of 2002.

- As a result of Austar's losses, UAP defaulted on interest repayments required under various senior debt notes. The principal creditors of UAP at the time of the Application were approximately seventy bondholders, unrelated to the parties to this proceeding.

- Accordingly, UAP sought to restructure its US-based debt by means of a United States Chapter 11 bankruptcy procedure. The Chapter 11 procedure broadly resembles the Australian scheme of arrangement procedure set out in Chapter 5 of the Corporations Act with a mandatory moratorium applying from the time a Chapter 11 application seeking relief from creditors is filed with the bankruptcy court.

- On 20 December 2002 (US Time)1 CHAMP SPV Pty Limited, a subsidiary of CHAMP, and UAH entered into a Master Agreement and Reorganisation Agreement (together, CHAMP Agreements), performance of which was conditional, amongst other things, on the Chapter 11 procedure being approved by the relevant creditors and court.

- Under the CHAMP Agreements, CHAMP and its related entities would pay UAP US$34.5 million (approximately A$61.0 million), which amount would be used by UAP in satisfaction and cancellation of certain of UAP's creditors' claims. In exchange CHAMP SPV would acquire UAH's 63.2% shareholding in UAI, and therefore acquire joint control (with UAPC) of UAI's 80.7% interest in Austar.

- UAPC would continue to hold 36.8% of UAI and so would continue to have a relevant interest in UAI's 80.7% interest in Austar.

- Under sub-sections 608(3) and 608(8) of the Corporations Act2 , CHAMP SPV acquired a relevant interest in the 80.7% of Austar held by UAI when it entered into the CHAMP Agreements on 20 December 2002. On 20 December 2002, ASIC granted an exemption from section 606 (the 20% threshold) under section 655A to CHAMP Group permitting CHAMP SPV to enter into the CHAMP Agreements (ASIC Relief).

- The ASIC Relief was conditional on CHAMP Group making takeover offers for the 19.3% of shares in Austar held by UAPC and the public within 4 weeks of the Chapter 11 procedure taking effect. The offer is required to be made at a price no less than the effective see-through price for the 80.7% parcel (i.e. the US$34.5 million is treated as the price of 63.2% of 80.7%, subject to minor adjustments).

- UAI, CHAMP SPV and UAPC also entered into a shareholders agreement on 23 December 2002 (US Time)(Shareholders Agreement). This governs the future relationship of the UGC Group and the CHAMP Group in respect of their investments in UAI and Austar and sets out their agreement on the composition of Austar's management and board.

- The Shareholders Agreement contains provisions relating to, amongst other things:

- The number of CHAMP Group and UAPC nominee directors elected to the Austar board;

- Future independent directors on the Austar board;

- The chairmanship of the Austar board;

- The CEO of Austar;

- The make-up of the underwriting agreement for a proposed future rights issue by Austar;

- Restrictions on transfer of Austar shares controlled by CHAMP Group and UAPC;

- Management fees in relation to Austar; and

- Standstill agreements between UAPC and CHAMP Group.

- On 23 December 2002 (Australian time), CHAMP Group lodged a Notice of Initial Substantial Shareholder under section 671B (Initial Notice), disclosing a relevant interest in 80.7% of Austar. Both CHAMP Agreements were attached to the Initial Notice. The Initial Notice did not attach the Shareholders Agreement, which was signed on 23 December (US time) (i.e. 24 December (Australian time)).

- On 18 February 2003, CHAMP Group lodged an amended Notice of Initial Shareholder disclosing that UAPC was its associate and had a relevant interest in 0.6% of Austar. On that basis CHAMP Group advised that it had voting power in 81.3% of Austar3 . CHAMP Group lodged a further amended Notice of Initial Shareholder on 20 February 2003 stating that CHAMP Group had voting power in the 0.000196% held by a director of the CHAMP Group. These notices are referred to together as Subsequent Notices.

- On 23 January 2003, (almost a month after the CHAMP Group announcements and first substantial shareholding notice), Pondale acquired 3,000 shares in Austar for $622.

- On 28 February 2003 the Panel received an application from Pondale, which forms the basis for these proceedings.

Application

- Pondale's Application raised four issues.

A. Ownership and Control of CHAMP Group

- Pondale asserted that the market and Austar shareholders were inadequately informed about the ownership and control of the CHAMP Group. Pondale alleged that the information contained in the Initial and Subsequent Notices did not contain sufficient information as to who ultimately controlled CHAMP Group or regarding the relationships between the various entities in the CHAMP Group. Pondale asserted that the ultimate ownership and control of the CHAMP Group (to the extent that additional entities had a relevant interest in the Austar shares) should be disclosed.

B. Disclosure of the Shareholders Agreement

- Pondale asserted that the Shareholders Agreement (as well as the CHAMP Agreements) was a `relevant agreement' for the purposes of section 671B(4)(a) and should have been attached to the Initial Notice or the Subsequent Notices4 .

- Pondale submitted that the Courts have held that once a relevant agreement is found to have contributed to the situation requiring a notice under section 671B, it is not necessary to consider the quality or degree of that contribution5 .

C. Difference between percentage exempted under ASIC Relief and CHAMP Group Substantial Shareholding Notices

- The ASIC Relief applied to the acquisition by CHAMP Group of a relevant interest in UAI's 80.7% holding in Austar. The ASIC Relief made no reference to the acquisition by CHAMP Group of a relevant interest in two parcels of Austar shares in which CHAMP Group's associates had relevant interests. On the basis that these parcels fell outside the ASIC Relief, Pondale asserted that the CHAMP Group contravened Section 606(1) because its voting power included its associates' relevant interests in these parcels.

D. CHAMP Group's Intentions for Austar

- Pondale asserted that the market for control of Austar was uninformed because the CHAMP Group had not made detailed disclosures about its intentions for the future of Austar. Pondale asserted that, as the relevant interest arose when the CHAMP Agreements were executed, it was unsatisfactory that these disclosures would not be until the follow-on bid was made.

Orders sought

- Pondale did not identify the orders, which it sought to be made by the Panel.

Panel considerations

A. Ownership and Control of CHAMP Group - Interests in Austar shares

- After the Panel had commenced the Austar Proceedings and given a brief to the parties, the CHAMP Group issued a detailed media release on 5 March 2003 dealing, amongst other things, with the ownership and control of CHAMP Group.

- On 13 and 14 March 2003 the controlling shareholders of CHAMP (the 100% parent of CHAMP SPV) gave substantial shareholding notices, concerning their substantial holding in Austar as owners of more than 20% each of CHAMP.

- The Panel considered that the media release and the substantial shareholding notices given by owners of CHAMP adequately disclosed their interests and substantial holdings in the Austar shares. Hence, there was no longer a need for the Panel to take action to remedy their failure to lodge substantial shareholding notices in December 2002. The Panel concedes that there may be a view that CHAMP's shareholders were not required to give substantial shareholding notices on 23 December 2002. However, the Panel considers that the better view was that disclosure was required.

- The funding structure that the CHAMP Group put in place to fund the acquisition of the interests in the Austar shares included a number of Belgian limited liability companies. The identities of the investment companies were disclosed in the CHAMP Group substantial shareholding notices of 23 December 2002 but there was no disclosure of the investors in the funds that invest in the investment companies.

- The CHAMP Group advised that the investors in the CHAMP Group's investment funds would not have relevant interests in the Austar shares and hence that the Corporations Act did not require their identity to be disclosed. CHAMP Group advised that the investors would all be passive investors that did not have any degree of control over CHAMP Group. Further, CHAMP Group's advice as to the dispersed ownership of the investment funds supported its claim that substantial shareholding notices were not required from those investors.

- Changes in the structure or relationships of the CHAMP Group or the investment funds may bring about different disclosure requirements in the future, but that is not a question currently before the Panel.

B. Disclosure of the Shareholders Agreement

- Having entered into the CHAMP Agreements on Friday 20 December 2002 (US time), CHAMP SPV was required to lodge the Initial Notice on or before the end of Tuesday 24 December 2002. It lodged the Initial Notice on Monday 23 December 2002 at 2.00 p.m. or thereabouts (Sydney time).

- The Panel accepted that the Shareholders Agreement had not been executed at the time the Initial Notice was lodged. It considered that the parties' intentions and obligations to enter the Shareholders Agreement and the negotiations and settling of terms for that had contributed to the situation giving rise to CHAMP needing to provide the Initial Notice when the obligation to do so was originally created. Further, it considered it highly likely that the material terms of the Shareholders Agreement were sufficiently well developed at that time that section 671B(4)(b) required CHAMP SPV to attach a statement giving full and accurate details of the terms of the proposed Shareholders Agreement to the Initial Notice.

- Clause 4 of the Master Agreement states that the parties were required to enter into the Shareholders Agreement within 3 days of signing the Master Agreement i.e. by 23 December 2002 (US time). Entry into the Shareholders Agreement was also a condition precedent of the Master Agreement. The Panel considered that it is implausible that the CHAMP Group would have entered into the Master Agreement under which it: without contemporaneously negotiating at least a substantial portion, and in particular the key terms, of the Shareholders Agreement.

- acquired a relevant interest in 80.7% of Austar; and

- invested $US34.5 million into UAI,

- In its supplementary disclosures by way of media release dated 5 March 2003, the CHAMP Group disclosed a summary of aspects of the Shareholders Agreement. The owners of CHAMP attached a copy of the Shareholders Agreement to their substantial shareholding notices dated 13 March 2003.

- The Panel considered that the CHAMP Group, or the owners of CHAMP, are likely to have been in breach of the substantial shareholding provisions, and acting contrary to the principle set out in section 602(a), for nearly 3 months. However, as they volunteered to make full disclosure once they fully understood the Panel's interpretation of section 671B(4)(b), the Panel was not required to decide whether or not to make a declaration of unacceptable circumstances in relation to this issue.

- The Panel considers that:

- where a transaction is effected by various connected agreements; and

- the obligation to give a substantial shareholding notice is triggered by entry into the first agreement,

- The person giving the substantial shareholding notice must be in a position to explain why, having entered the triggering agreement, the parties have not reached sufficient consensus on the terms of the other agreements to bring section 671B(4)(b) into play. Thus, it is likely that the decision in New Ashwick will in many cases require the disclosure of the related agreements (or a summary of those parts of the agreement that have been agreed and a description of the other provisions that are intended to be included in the agreement) even if the agreement creating the relevant interest is executed before the other agreements have been finalised.

C. Difference between percentage exempted under ASIC Relief and CHAMP Group Substantial Shareholding Notices

- As noted above, the ASIC Relief did not apply to the acquisition by CHAMP Group of relevant interests in the two parcels of Austar shares owned respectively by UAPC and a director of the CHAMP Group.

- UAPC's direct holding of 0.6% of the shares in Austar is included in CHAMP Group's voting power, because entering the CHAMP Agreements made UAPC and CHAMP become associates in relation to Austar. The CHAMP Agreements and the Shareholders' Agreement provide expressly that CHAMP Group has no control over voting or disposal of UAPC's 0.6% parcel. There is obviously some tension between these provisions and the overall relations between CHAMP Group and UAPC, but there was no submission and no evidence that the clauses were shams. Accordingly, the Panel takes them at face value and infers that CHAMP Group did not acquire a relevant interest in UAPC's direct 0.6% holding by entry into the CHAMP Agreements and the Shareholders Agreement, but was nevertheless required to include these in its Initial Notice.

- On its face, the ASIC Relief is effective, although entry into the CHAMP Agreements and the Shareholders Agreement resulted in CHAMP Group's voting power including UAPC's additional 0.6%.

- The existence of UAPC's direct holding and the effect on that parcel of entry into the CHAMP Agreements and the Shareholders Agreement were disclosed to ASIC before the ASIC Relief was granted In its submission to the Panel, ASIC stated that the relief was intended to operate that way:

"The [0.6%] Parcel was intentionally not covered by the instrument issued by ASIC. This is because the Direct Parcel is held by a separate upstream entity outside the CHAMP Group, i.e. UAPC, therefore ASIC considered it appropriate that the Direct Parcel be the subject of the "downstream" bid by CHAMP. "

- Since the ASIC Relief applied, and was intended to apply, despite the addition of the 0.6% parcel to CHAMP Group 's voting power, that circumstance is not unacceptable.

D. CHAMP Group's Intentions for Austar

- As the ASIC Relief requires CHAMP Group to make takeover offers for the publicly held shares in Austar and UAPC's shares in Austar, the Panel considered that the proper time for the CHAMP Group to make such disclosures is when it issues its bidder's statement. The Panel considered that in the present circumstances, the market and Austar shareholders have been properly informed of CHAMP Group's substantial shareholding and of the requirement in ASIC's Relief for a follow-on bid.

Pondale's Standing

- A fundamental issue for the Panel is that it know the identity of all applicants. The small size of Pondale's shareholding in Austar and the timing of its acquisition raised concerns about Pondale's motivation for making its Application. The Panel therefore sought information from Pondale, and its solicitors, as to whether any other person had given instructions to Pondale in relation to its Application.

- Pondale advised the Panel and parties to the application that a client of Watson Mangioni, Wattle Park Partners Pty Ltd (WPPPL), requested Watson Mangioni to acquire shares in Austar, to acquire those shares through a vehicle connected with Watson Mangioni (i.e. Pondale), and to make the Application. WPPPL agreed to pay all of Pondale's costs in connection with the Application.

- A confidential submission sent to the Panel by Watson Mangioni (Confidential Submission) (but not provided to the parties) stated, amongst other things, that WPPPL wished to obtain additional information about the ownership and control of the CHAMP Group. It disclosed information about WPPPL's industry connections, including its retainer from Seven Network Limited (Seven) to advise Seven on telecommunications and media matters, which indicated an explanation as to the underlying motivation for the Application. Pondale purchased the Austar shares to enable it to activate the tracing procedures of Part 6C.2 of the Corporations Act and, when the information provided via this process failed to satisfy WPPPL, to make an application to the Panel. WPPPL asserted that the Application was a legitimate way of seeking information about the ultimate ownership and control of CHAMP Group. The Confidential Submission stated that Seven was aware of the Application. However, Pondale gave none of this information to the Panel in its initial Application.

- For procedural fairness reasons the Panel will not make use of documents in relation to which other parties do not have an opportunity to comment. Not until the Panel's decision was made on 18 March 2003 did the sitting Panel members view the Confidential Submission for the purposes of deciding how much of the information should be disclosed in the Panel's reasons. Hence, the confidential information was not relied on as evidence on the substantive issues in the proceedings, or any of the matters on which CHAMP Group had to defend itself. Its relevance was limited to Watson Mangioni having provided it by way of response to a submission that Pondale and it were abusing the process. The Panel had directed the Panel Executive to read the Confidential Submission from Watson Mangioni and advise of its nature, but not actual content, in order to decide how to deal with the document.

- The Panel seriously considered declining the Application when advised of the instructions behind Pondale's Application. However, as Pondale formally had standing, the Panel decided to consider whether the issues raised by the Application would properly be of concern to the market generally or to Austar shareholders in particular. The Panel decided that at least two of the issues raised were, of themselves, sufficiently material to the market for Austar shares to proceed with the Application, regardless of the concerns the Panel had in connection with the underlying motivation for Pondale's Application.

Decision

- The Panel declined Pondale's Application. It consented to the parties being represented by their solicitors.

Dated 4 June 2003

Nerolie Withnall

President of the Sitting Panel

In the Matter of Austar

APPENDIX A

1 i.e. Saturday 21 December 2003 (Melbourne time).

2 All references to sections in this document refer to the Corporations Act.

3 UAPC's direct holding of 0.6% of the shares in Austar is included in CHAMP Group's voting power, because entering the CHAMP Agreements made UAPC and CHAMP Group become associates in relation to Austar.

4 Section 671B(4)(a) provides that a notice under that section must be accompanied by "a copy of any document setting out the terms of any relevant agreement that contributed to the situation giving rise to the person needing to provide the information" under Section 671B(3).

5 New Ashwick Pty Ltd v Wesfarmers Ltd (2000) 35 ACSR 263 (New Ashwick). However, in considering the issues in these proceedings the Panel considered that it should only require disclosure of documents where the contribution is material and the information disclosed would reasonably and materially assist the market for Austar shares.